This article first appeared in Capital, The Edge Malaysia Weekly on September 26, 2022 - October 2, 2022

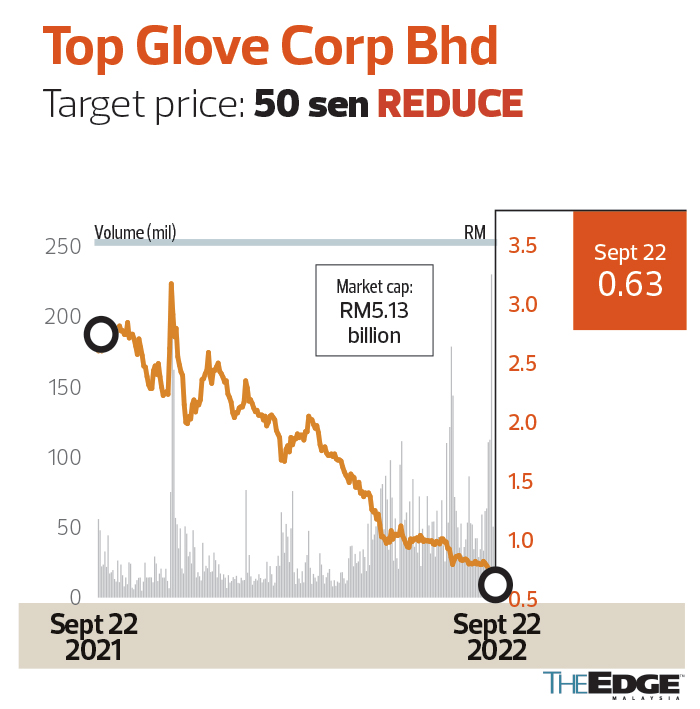

Top Glove Corp Bhd

Target price: 50 sen REDUCE

CGS-CIMB RESEARCH (SEPT 20): Top Glove’s 4QFY8/22 core net profit came in at RM3.4 million, excluding losses of RM56 million. This brought FY8/22 core net profit to RM465 million — above expectations, ahead by 155% of our and 153% of Bloomberg consensus’ FY22 estimates. The earnings beat was due to a surprise new revelation by Top Glove that it had conducted an inventory write-down of RM229 million in FY22. No dividend was declared in the quarter.

Heading into FY23F, we expect Top Glove to post a 90% year-on-year (y-o-y) dip in core net profit, assuming average selling prices (ASPs) of US$19 per 1,000 pieces and a utilisation rate of 50%. Note that we expect the supply glut in the global glove sector to only dissipate towards 2HFY23F. While Top Glove intends to raise its ASPs by 5% in October 2022 to pass on cost hikes, this is likely to be difficult in the near term, given the current operating environment where the industry utilisation rate remains low at 40% to 45%, while ASPs currently stand at US$18 to US$20 per 1,000 pieces.

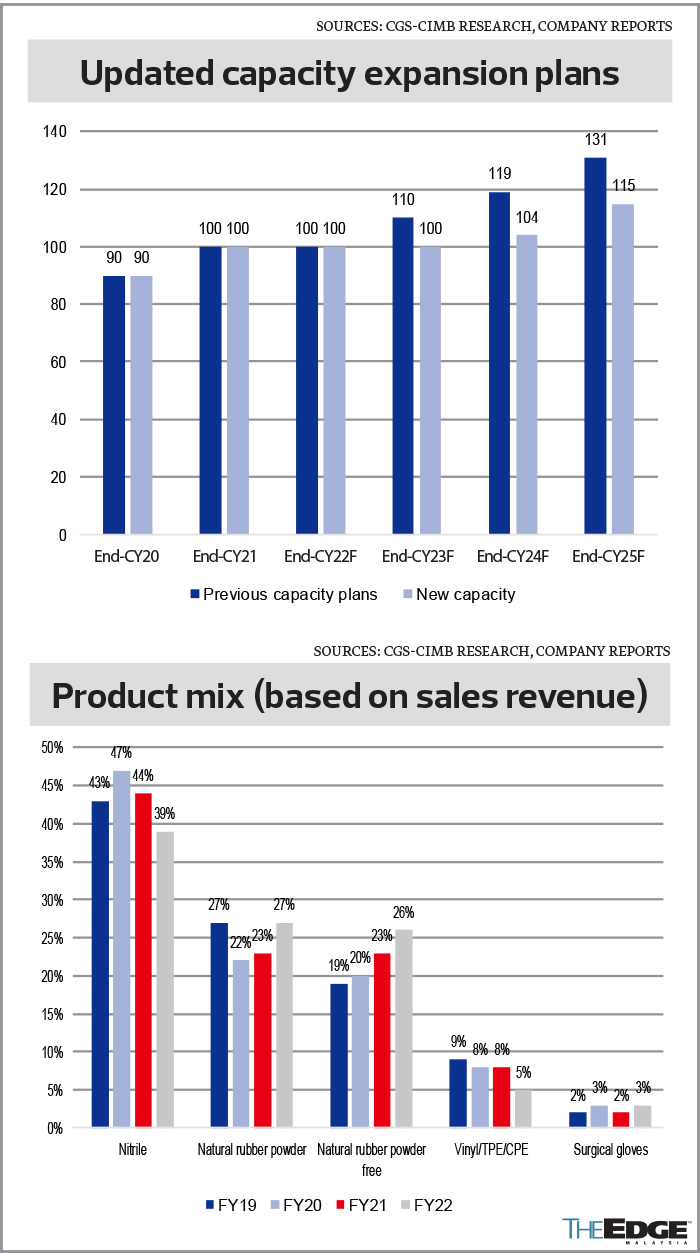

In view of the current weak operating environment, Top Glove is deferring its capacity expansion plans in 2023F. It is only expecting to grow its annual capacity by 4% (additional four billion from current capacity) in 2024 and 11% (additional 11 billion from current) in 2025. In total, it has deferred a total of 31 billion in new capacity that it intended to add by end-CY25F. We view this positively as it will alleviate pressure on Top Glove to sell its new capacity, on top of the positive impact on overall global glove supply-demand dynamics.

We lower our FY23-24F EPS by 60% to 86.5% to account for lower-than-expected sales volume and weaker ASPs. Accordingly, our target price is lowered to 50 sen. We keep our “reduce” call as current valuations have yet to fully account for its weak near-term earnings prospects.

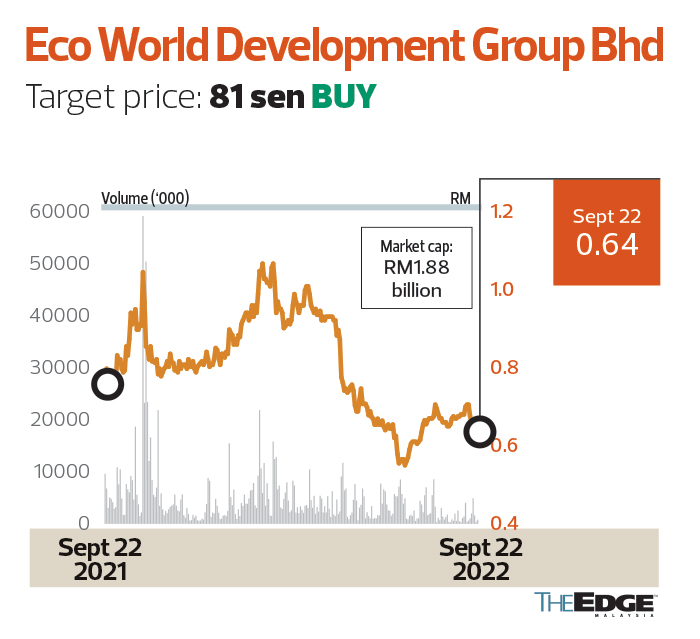

Eco World Development Group Bhd

Target price: 81 sen BUY

MAYBANK INVESTMENT BANK RESEARCH (SEPT 18): Excluding RM1.3 million one-off (including the reversal for impairment of right-of-use assets and allowance for impairment of receivables), ECW reported a 3QFY22 core net profit of RM45.1 million, lifting 9MFY22 core earnings to RM149.4 million, accounting for 64% of MIBG FY estimates and 66% of consensus estimates. ECW’s 4QFY22 earnings should be seasonally stronger. Also, its 27%-associate Eco World International Bhd (ECWI) is expected to report profit in 4QFY22 with the delivery of two UK projects.

ECW has locked in RM3.4 billion in property sales in 10MFY22, accounting for 98% of its FY22 sales target of RM3.5 billion — exceeding expectations. Of the RM3.4 billion sales, 55% were derived from the central region, followed by Johor (31%) and Penang (14%). As at end-August, unbilled sales (for Malaysia projects) were RM3.95 billion or 1.2 times of our FY23E revenue. ECW has declared a second interim dividend of one sen.

Elsewhere, net gearing continued to improve to 0.35 times as at end-3QFY22, from 0.36 times at end-2QFY22.

We adjust FY22/23/24 earnings forecasts by -5.6%/+4.4%/+6.6% to factor in: (i) a higher FY22 property sales assumption of RM3.8 billion; and (ii) new ECWI loss projections.

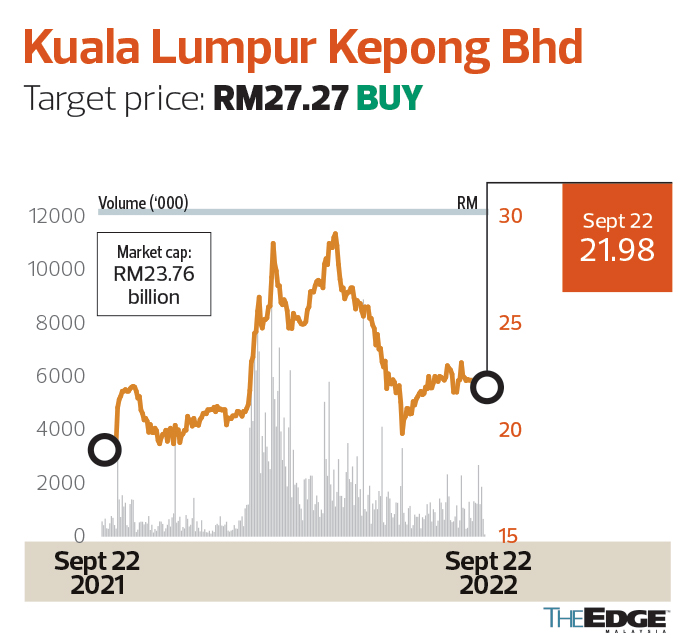

Kuala Lumpur Kepong Bhd

Target price: RM27.27 BUY

HONG LEONG INVESTMENT BANK RESEARCH (SEPT 20): KLK’s 10MFY22 fresh fruit bunch (FFB) output grew 27% to four million tonnes, boosted mainly by contribution from IJM Plantations Bhd. Management guided that FFB output growth will sustain for the next two to three months, on the back of seasonal factors.

Moving into FY23, we understand that FFB output will grow further and hit FFB yield of 21.5 tonnes per ha, on the back of easing foreign labour constraints in the Malaysian operations alongside continuation of mechanisation efforts.

KLK’s ex-mill CPO production cost fell by 3% quarter on quarter to RM1,940 per tonne, due mainly to higher FFB output. Management guided that CPO production cost will increase further to RM2,000 per tonne in FY22, due to higher fertiliser prices and application. It is expected to increase further in FY23, due to higher fertiliser costs and the full impact of the minimum-wage hike on the Malaysian operations, but partly mitigated by higher FFB output.

We expect the manufacturing segment’s performance to improve in 4QFY22, on the back of relaxation of export curbs in Indonesia. Contribution from the property development segment will remain stable, supported by property launches in small phases.

We maintain our “buy” rating on KLK, with a higher SOP target price of RM27.27. KLK remains one of our top picks for the sector, given its decent valuations.

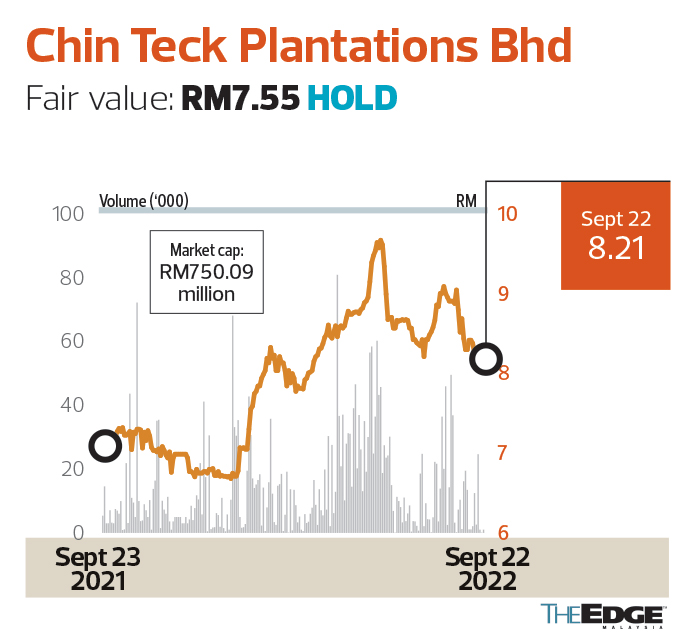

Chin Teck Plantations Bhd

Fair value: RM7.55 HOLD

AMINVESTMENT RESEARCH (SEPT 20): Recently, CTP proposed to acquire Fauzi-Lim Plantation (FLP) for RM45 million from MWE Holdings. FLP has a lease for 2,023ha of oil palm estates in Gua Musang, Kelantan, from Yayasan Islam Kelantan. The tenure of the lease is from July 28, 1999 to July 27, 2065 with an option for another 33 years. The proposed acquisition is expected to be completed by Dec 31, 2022.

We are neutral on this development. We do not expect earnings contribution from the new land bank to be significant. We believe that FLP’s production costs are high due to low FFB yields. FFB production was only 3,250 tonnes in FYE3/22 with the age of oil palm trees between 21 and 22 years old. FLP recorded a net loss of RM0.7 million in FYE3/21.

The proposed acquisition of FLP will expand CTP’s planted areas by 17% to 12,822ha. However, as the land is leased from Yayasan Islam Kelantan, CTP will not own the oil palm estates.

The proposed acquisition price of RM45 million translates into RM24,168 per ha based on FLP’s planted areas of 1,862ha. We think that the purchase price is low compared to oil palm estates in Sabah or Johor as the land will be leased from another party.

Also, the oil palm trees are ageing. The net book value of CTP’s oil palm trees in Gua Musang, Kelantan, was RM13,519/ha as at end-August 2021. CTP has 1,618ha of oil palm trees in Gua Musang.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.