This article first appeared in The Edge Malaysia Weekly on November 15, 2021 - November 21, 2021

AS the measure that gives financially distressed public-listed companies (PLCs) a temporary reprieve from being classified as a Practice Note 17 (PN17) and Guidance Note 3 (GN3) listed issuer ends in less than two months, Bursa Malaysia says there will be no more blanket extension. However, applications for further extension will be considered on a case-by-case basis.

In view of the government’s decision to open up all economic sectors with over 95% of the country’s adult population fully vaccinated along with the reducing rate of new Covid-19 cases, a spokesperson for Bursa says the market regulator has no plans to extend the existing temporary relief measures any further.

“But if there are any applications by [affected] companies for a further extension of the existing relief measures, Bursa could consider such applications on a case-by-case basis,” the spokesperson says in an email response to questions from The Edge.

While it is clear some companies have benefited from the reprieve as they are given more time to regularise their financial condition, it has also drawn criticism that the regulatory authorities are simply propping up companies with a low chance of survival.

In April last year, when the Covid-19 pandemic hit, Bursa and the Securities Commission Malaysia (SC) introduced the waiver as part of a package of measures aimed at alleviating the impact of Covid-19 on businesses. Under the waiver, companies that triggered any of the suspended criteria between April 17, 2020, and June 30, 2021, would not be classified as a PN17 and GN3 company for 12 months.

The waiver has been extended twice since then, with the latest extension granting companies that trigger the PN17 or GN3 suspended criteria between July 1, 2021, and Dec 31, 2021, an 18-month relief period, compared with 12 months previously.

The SC’s Annual Report 2020 shows that a total of 13 companies benefited from the relief measure in 2020, and AirAsia X Bhd (AAX) was one of them. However, the low-cost, long-haul carrier slipped into PN17 status last month after triggering a non-PN17 suspended criterion when its external auditor, Messrs Ernst & Young PLT (EY), expressed a disclaimer of opinion on its accounts for the 18 months ended June 30, 2021.

The carrier has been loss-making since the financial year ended Dec 31, 2018 (FY2018) and in October 2020 filed a plan to restructure RM63.5 billion of its debt, which was reduced to RM33.65 billion after a proof of debt exercise conducted by AAX to determine and finalise the list of scheme creditors and the value of their scheme amount. Last Friday (Nov 12), AAX managed to obtain a near-unanimous approval for its debt restructuring scheme from its creditors, which would enable a proposed corporate restructuring and RM500 million fundraising to proceed.

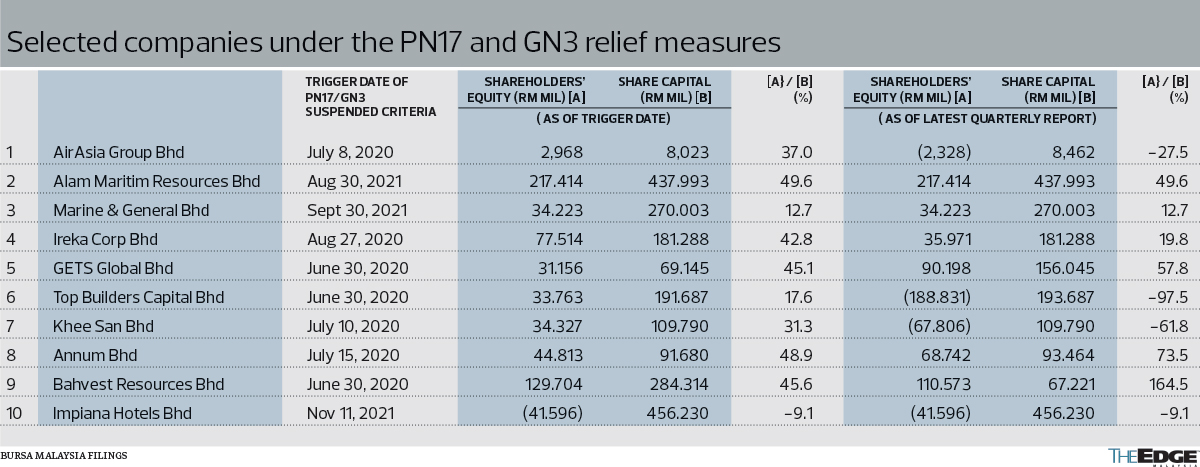

A check on Bursa by The Edge shows companies that have managed to stave off relegation to the PN17/GN3 category until well into 2023 include AirAsia Group Bhd, Alam Maritim Resources Bhd, Marine & General Bhd, Ireka Corp Bhd, GETS Global Bhd, Top Builders Capital Bhd (formerly Ikhmas Jaya Group Bhd), Khee San Bhd, Annum Bhd (formerly Cymao Holdings Bhd), Bahvest Resources Bhd and Impiana Hotels Bhd.

Andrew Heng, group managing partner at Baker Tilly Malaysia, says the relief measures for listed issuers that were announced by Bursa and the SC came swiftly and at the right time when companies were battling with the challenges in both safety concern from the deadly virus while juggling to deal with the negative business impact from economic lockdowns over the last two years.

“These relief measures are welcomed by listed issuers in Malaysia, as it not only allows more time for them to submit their financial statements, but for certain companies that were badly hit to have the breathing space to restructure their Covid-19-affected business to avoid suspension and delisting amid the pandemic,” he tells The Edge.

“The relief measures had definitely helped entities, especially those that operate in the industries that are most impacted by the Covid-19 pandemic such as airline, leisure, travel and hotel industries, as these entities were shut or were not allowed to operate in full capacity in light of the Movement Control Order during the pandemic.

“If I were to single out a particular relief that I think is most effective or fit for purpose, it would be the period of relief granted to listed issuers with inadequate levels of operations from triggering of any PN17/GN3 suspended criteria between July 1, 2021, and Dec 31, 2021. This is because certain entities could have triggered this suspension criterion purely as a consequence of the economic lockdown, which is a global crisis,” he says.

“The suspended criteria — which include the criteria on shareholder’s equity, the ability of the listed issuers to continue as a going concern and the default in payment — are closely linked to the performance of the listed issuers. Without the relief measures on these suspended criteria, I believe that there will be more affected entities classified as PN17/GN3 due to low or even zero revenue during this economic lockdown. Hence, the relief measures are vital to provide a space for the affected listed issuers to resolve their affairs, to regularise their temporary unsatisfactory condition and to restructure their bank borrowings, during this unprecedented time in history,” notes Heng.

There were 20 companies classified as PN17 and two under GN3, representing 2.43% of 905 companies listed on Bursa’s Main Market and ACE Market as at Nov 1, 2021.

Minority Shareholders Watch Group (MSWG) CEO Devanesan Evanson concurs, noting that granting relief periods to listed issuers that trigger the suspended PN17 or GN3 criteria was the right thing to do based on the context at that time.

He observes, however, that the extension of time has not been of much help due to the lingering effects of the pandemic and the numerous and prolonged lockdowns, which saw businesses suffer, financiers and “white knights” hesitant, and fundraising opportunities dry up.

“The end was never in sight and that uncertainty further exacerbated the recovery process,” he says.

The Bursa spokesperson says it is of the view that the non-classification as a PN17 or GN3 company for the relief period had allowed the affected listed companies to focus their efforts on sustaining and improving their business, operations and financial condition during this challenging period without additional regulatory burden.

“As of today, there are 13 affected issuers benefiting from our relief measures. Moving forward, all listed issuers are expected to fully comply with the provision of listing requirements,” the spokesperson says.

Calling a spade a spade

Bursa’s decision not to extend the PN17/GN3 waiver would come as welcome news to MSWG, which has maintained that companies that trigger the PN17 criteria should continue to be classified as one.

“In ‘substance’, they are PN17 and going about calling them not-PN17 is an exercise in ‘form’. Some minority shareholders may actually end up investing in these PN17 companies that are financially distressed as they are not flagged out as PN17 companies. In this regard, the investors cannot make an informed decision. In short, classify them for what they are (a PN17 company) and at the same time, help them with the extensions of time and other concessions. Substance should prevail over form,” Devanesan tells The Edge.

Baker Tilly Malaysia’s Heng concedes that the unintended consequence of the PN17/GN3 waiver is that some listed issuers, who had already performed poorly before the pandemic, may have escaped the suspension, and shareholders’ interests may not have been safeguarded in this circumstance.

“For example, badly managed listed issuers may have accumulated significant losses or low shareholders’ equity amounts even before the pandemic. In my personal view, setting additional conditions, such as only certain industries that are badly affected by the pandemic can enjoy this relief measure, may help to address this unintended consequence,” he says.

In MSWG’s weekly newsletter dated Aug 14, 2020, Devanesan highlighted that some companies had already shown signs of trouble brewing even way before the pandemic. “Thus, the current health crisis might as well be made a scapegoat or escape route to legacy issues faced by those companies that triggered the PN17/GN3 criteria,” he said.

He cited GETS Global as an example, which had posted several quarters of losses before the pandemic hit. “Meanwhile, candy maker Khee San has long been known for its default on multiple loan payments and is in litigation with banks to resolve its issues,” he added.

‘Keep the relief measures, but fine-tune them’

It remains to be seen whether the relief measures, such as the temporary waiver from being classified as a PN17 company, have helped to put listed companies on a better footing than the earlier stages of the pandemic. This may not seem the case thus far judging by the list of affected PLCs compiled by The Edge, which showed that the percentage ratio of the shareholders’ fund over their respective share capital has mostly remained below the 50% threshold that otherwise would have triggered the PN17 criteria, even after being granted the waiver (refer to the table above).

It is still too early to say, according to Heng.

“As to whether any companies are better off financially today, it may be too early to judge at this juncture as the country is still trying to recover from the pandemic as businesses gradually open. As of today, international borders have remained closed except for certain approved travel,” he says.

“Many entities, for example, the airline and hotel operators that have been severely impacted by the pandemic, are still suffering from the negative effects because of the pandemic and will take time to fully recover.

“The ripple effects are still unfolding, and it is unlikely that the true impact of this pandemic can be measured until the situation stabilises,” he adds.

Heng believes Bursa and the SC should continue to grant further extension of the waiver to listed issuers as part of the National Recovery Programme, but it should fine-tune the relief measures to be industry-specific rather than a “free for all” for all entities.

“The extension of the relief should be for all entities in the selected industries, without the need to submit an application for such relief measures. We all understand how complicated the application can be in seeking relief, especially in trying to justify that the business is still affected by Covid-19.

“The economy in Malaysia is still recovering. Many businesses have only just been allowed to operate recently, that is, in the last quarter of 2021. It is still too soon to tell. In short, the waiver is still very much needed for those affected listed issuers in order for them to resolve their affairs, to regularise their temporary unsatisfactory condition to recover from the Covid-19 pandemic and to return to its pre-pandemic trend,” he says.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.