This article first appeared in City & Country, The Edge Malaysia Weekly on June 7, 2021 - June 13, 2021

The third prolonged lockdown in the UK has had an impact on what people want from their property, which will lead to continued price growth across the prime markets beyond London, especially in the country house and coastal markets, where there is the greatest imbalance in supply and demand, according to a Savills UK webinar held on May 27.

The panellists concurred that longer-term price growth across all markets will be supported by a low interest rate environment, although this will be tempered by the prospect of higher taxes as the government seeks to restore public finances. The panellists were head of residential research Lucian Cook and residential research associate director Frances Clacy.

Cook said that since last June, the number of monthly sales of £1 million-plus (RM5.8 million-plus) homes has been 60% to 90% above the levels seen between 2017 and 2019, and exceeded twice the level of normal market activity for the first time in April this year.

With the ability to lock into a low cost of borrowing, wealthy and financially secure households have had both the inclination and opportunity to respond to a reassessment of their housing preferences and needs. “While the lockdown in 1Q2021 caused some to put their plans on hold temporarily, prolonged social distancing appears to have embedded the changes in buyer priorities, at least in the short term. In March and April, deals being struck for the sale and purchase of £1 million-plus homes were again 94% and 112% above normal levels for the month,” he noted.

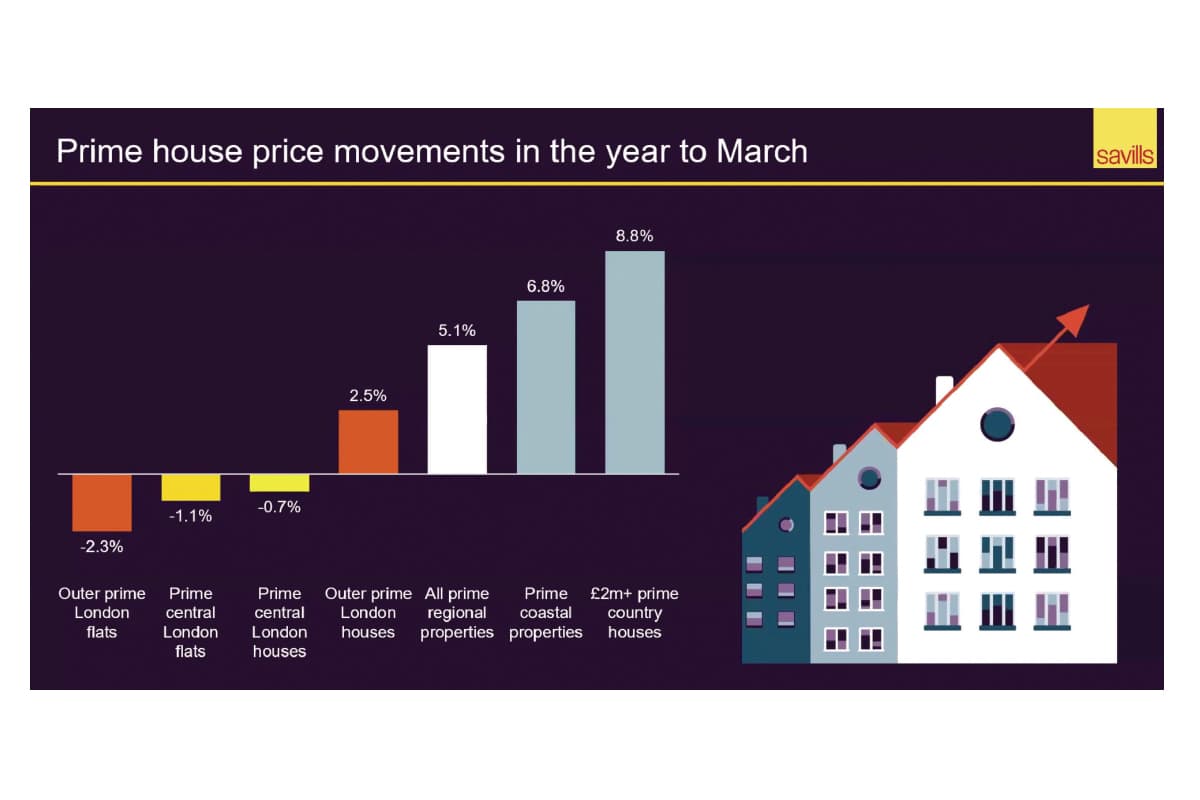

However, not all parts of the market have been equally affected by the pandemic, said Cook. “The reassessment of what people want and need from their home has generally favoured the country over London. Within London, they have preferred houses over flats.”

According to him, prices of £2 million-plus country houses increased by 8.8% in the year to end-March this year — remarkable for a market that was best described as quiet during the preceding decade. Whereas in South Oxfordshire, the epicentre of a resurgence in activities at the top end of the market, sales of £1 million-plus properties agreed from early June 2020 to end-April 2021 were 184% higher than the same period the year before.

“By any measure, activity in the markets beyond the capital has been exceptional. But, while not having quite the same level of intensity, the prime property market in London cannot be said to have fared badly. Here, needs-based markets, such as those of South West London, have benefited from a search for space among households that have yet to have their fill of London life. Consequently, the value of houses in this area rose by 3.4% last year, while the value of flats had eased marginally by -0.5%,” said Cook.

In the more discretionary market of central London, the lack of international travel has restricted overseas buying activity. “But, even though demand in this part of the market has become more reliant on domestic buyers and non-domiciled residents, our research shows that £4.08 billion was spent on £5 million-plus homes in the capital in the year to end-April. That is £600 million more than what was spent in 2019,” he explained.

Over the coming months, it is inevitable that the forces that have shaped the prime housing markets over the past year will start to change. “At end-June, the benefit of the stamp duty holiday will reduce significantly, before being removed entirely by end-September. However, the patterns of market activity last year suggest that the top end of the prime market is far less reliant on the stamp duty holiday than, say, the segment of the market between £500,000 and £1 million,” said Cook.

Instead, he believes two other factors will shape the prime markets over the remainder of this year. First, the level of buying activity last year has created shortages in the number of property available to be purchased across large parts of the market. This has led to an imbalance between supply and demand that he expects will underpin prices across the prime family housing markets through 2021.

Second, the vaccination programme and the consequential relaxation of social distancing will start to affect buyer and seller behaviour. “Our client survey results indicate that this will actually increase buyer commitment over the medium term. But it is also likely to bring more stock to the market, especially from downsizers and others who were reluctant to sell while risks from the Covid-19 pandemic were high. That should gradually ease some of the supply constraints that we are seeing,” said Cook.

“We entered the market with a relative shortfall in terms of the stock available to the market compared with the levels of demand that we saw early this year. In January and February, people thought they had missed the boat, owing to the coming expiry of the stamp duty holiday. However, we did see a strong level of sales activity of between 60% and 70% above normal, but perhaps not quite at the same heights as that seen last October and December.”

When the extension of stamp duty holiday was announced in March, people felt there was another opportunity to take advantage of it. “We came out of a lockdown — which probably suppressed the level of demand in January and February — that brought people back to the market and there was a further strong pickup in levels of activity, whereby the highest level of sales agreed for £1 million-plus properties since the start of the pandemic was achieved in April,” said Cook.

“What we did not see was the stock coming to the market to match the demand and, as such, irrespective of losing a little bit of momentum when the stamp duty holiday goes … there is still a bit of unmet demand that is expected to sustain the market through 2021.

“This is reflected in what has happened in May, also a relatively strong month, in which levels of activity were 80% above normal, perhaps not quite as intense as in April, considering that people were less likely to catch the end of the stamp duty deadline by agreeing to a sale in that particular month. Still, the disconnect between supply and demand has the potential to put a bit of further upward pressure on prices.”

“The stamp duty and political uncertainty had more of an effect in London, particularly in central London, so values here have remained on average 21% below the 2014 peak. This represents a very good value, particularly for those buying in foreign currencies. Thus, this market was ready for its recovery during early 2020, after more than five years of price falls. The pandemic sort of put that recovery on hold, but it does not appear to have dented the appeal of the city’s very best addresses,” she said.

“Buyers now are also taking advantage of the value that is on offer, especially British buyers and those who are based in the UK, even though this opportunity could close quite quickly when international travel resumes and more competition returns to the market.”

Clacy added that April was a strong month despite the introduction of an overseas stamp duty surcharge, and desire for more space was also apparent at the very top end of the market. “Areas such as South West London and West London had accounted for a higher proportion of those £5 million-plus sales than they did since early 2020. However, this price tag does remain a bit of a rarity within these markets, as the majority of demand is still concentrated within central London’s well-established districts such as Knightsbridge and Belgravia.”

Moreover, there has been renewed demand for urban living as bars, restaurants and shops reopen in the UK. Buyers are planning for the new normal, which is driving more buying interest in prime regional towns and cities.

Clacy said many people have become more aware of what they have been missing out on and many buyers are looking for homes in a more vibrant location. As a result, prime prices across these markets have kept pace with those in village and rural areas, with an average annual growth of 4.9% compared to 5.2%.

“Although it is understandable that young wealthy families see the desirability of urban living, there has been an increasing number of empty nesters who are looking for good access to restaurants, shops and leisure facilities. Many of these moves have also been prompted by a desire to be close to family, a trend supported by the results of Savills’ buyer and seller survey conducted in March this year,” said Clacy.

“However, this occurrence is actually part of a longer-term trend, where prime urban areas have tended to outperform. Since the credit crunch, prime property in cities and towns have seen values surpass their previous 2007 peak by 22% and 15% respectively. Meanwhile, those in villages reached this level again only at end-2020. Across rural areas, prime prices still remain 8% below this previous high point,” she added.

Looking ahead, Clacy said the value on offer in prime village and rural areas will continue to support prices across these markets. Just as importantly, the value gap between London and prime regional towns and cities will also continue to drive additional demand there, particularly from those looking for more space.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.