This article first appeared in The Edge Malaysia Weekly on December 6, 2021 - December 12, 2021

THE third quarter of 2021 (3Q2021) was undoubtedly tough for corporate earnings, with the imposition of a total lockdown from June 1 that continued in various forms until end-September throughout the country.

However, RHB Research in its 3Q earnings review report considers the latest quarterly results to be broadly in line with expectations considering the consequences of the longer-than-expected Movement Control Order 3.0. Its misses-to-beats ratio improved to 1.1 from 1.4 in the preceding June quarter.

CGS-CIMB Research concurs, stating that the earnings disappointment owing to the lockdown in the Klang Valley was not as bad as feared, with positive earnings surprises coming from the agribusiness and healthcare sectors.

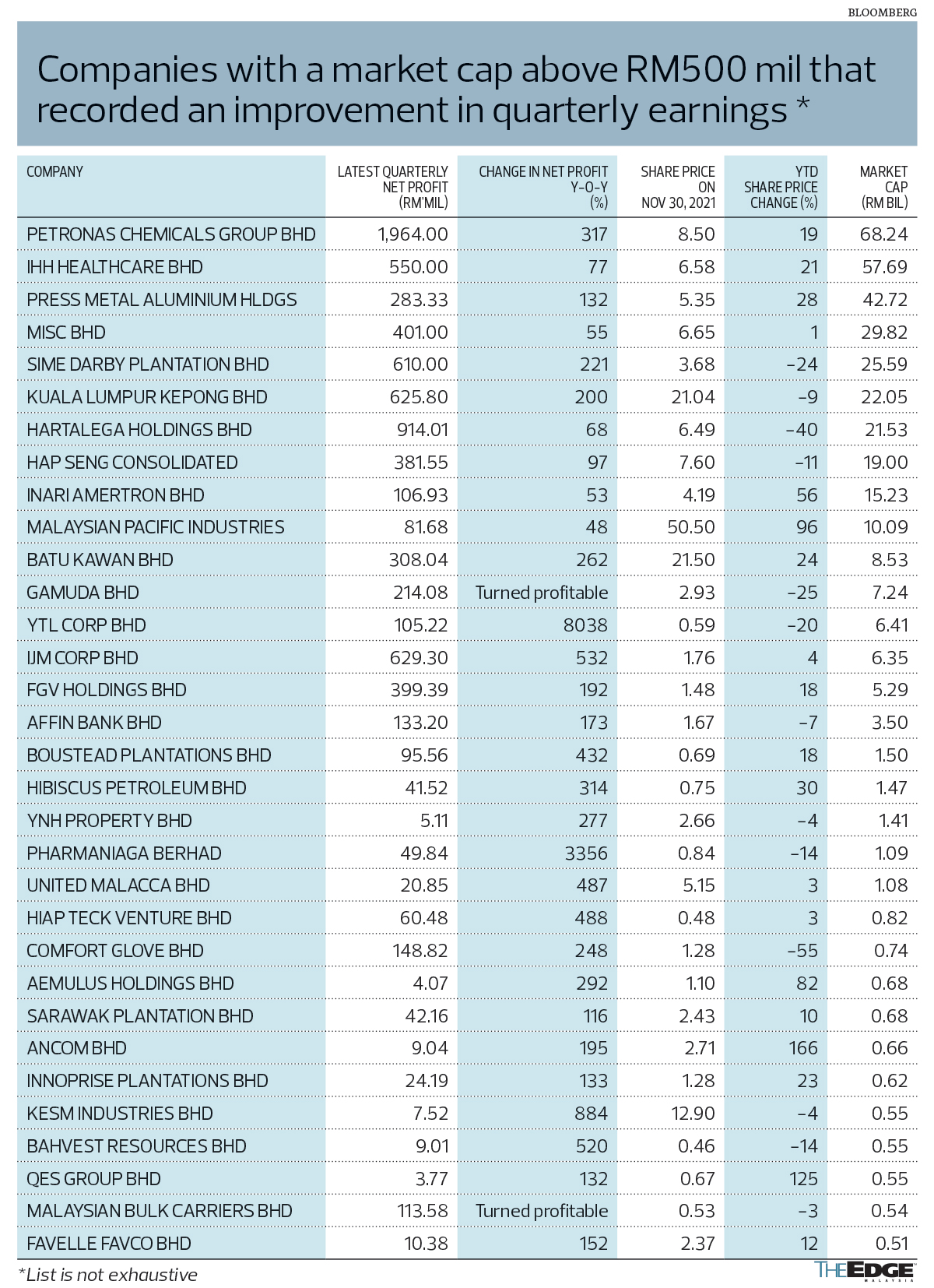

A quick check by The Edge on 269 companies listed on Bursa Malaysia with a market capitalisation of RM500 million and above shows that less than half or 129 of these companies recorded improved earnings in 3Q2021, while 140 reported a decline in earnings.

Improvements in earnings were mainly seen in commodity-dependent sectors, with higher crude palm oil (CPO) prices boosting the performance of plantation companies, and higher steel and aluminium prices helping companies dependent on those commodities. In contrast, the prolonged lockdown took its toll on some businesses, such as those in the retail and automotive sectors, forcing them to shut down during the period.

We look at how some of these companies performed in the past quarter.

SUPER BIG-CAP COMPANIES

(MARKET CAPITALISATION OF RM10 BILLION AND ABOVE)

Higher commodity prices helped boost the earnings of some super big-cap companies in 3Q2021. For one, soaring crude oil prices catapulted the net profit of Petronas Chemicals Group Bhd (PetChem) to a record RM1.96 billion in the third quarter ended Sept 30 (3QFY2021) from RM471,000 a year ago. Revenue increased 67% year on year (y-o-y) to RM5.77 billion, largely due to higher product prices in tandem with improving crude oil prices.

RHB Research in a Nov 23 note on PetChem said the group should see further earnings upside if the moderation in average selling prices is less steep than anticipated and PetChem is able to kick-start its Pengerang Integrated Complex project in Johor smoothly. The group’s refinery-petrochemicals complex in Pengerang was closed in March last year following a fire incident.

PetChem shares had appreciated 19% year to date (YTD) to close at RM8.50 last Tuesday, giving the company a market capitalisation of RM68.24 billion. RHB has a “buy” call on PetChem, with a target price of RM9.91.

Plantation companies Sime Darby Plantation Bhd (SD Plantation) and Kuala Lumpur Kepong Bhd (KLK) also saw an improvement in earnings during the quarter, thanks to higher CPO and palm kernel (PK) prices.

SD Plantation’s net profit more than tripled to RM610 million from RM190 million a year ago, while revenue grew 59% y-o-y to RM5.06 billion, thanks to higher average CPO prices, which increased 51% y-o-y to RM3,770 per tonne in 3QFY2021 while PK prices were up 66% y-o-y to RM2,274 per tonne.

Meanwhile, KLK’s net profit tripled to RM625.8 million in its fourth financial quarter ended Sept 30 (4QFY2021) from RM208.82 million in 4QFY2020, on the back of a 48% y-o-y increase in revenue to RM5.93 billion, thanks to a 52% y-o-y rise in CPO selling prices to RM3,631 per tonne and higher PK selling prices, which increased 58.4% y-o-y to RM2,213 per tonne.

Despite the stellar performance, RHB Research in a Nov 11 note maintains its “underweight” call on the plantation sector.

“Malaysia’s CPO output rose slightly (+1.3% month on month) to 1.72 million tonnes in October, while stocks increased 4.4% to 1.83 million tonnes, bringing the stock/usage ratio back to the historical average. We continue to expect next year’s fundamentals of supply to improve, with a moderation of CPO prices in 2022. We advise investors to ride the wave and look for opportunities to sell into strength,” said the research firm.

Press Metal Aluminium Holdings Bhd saw its net profit for 3QFY2021 more than double y-o-y to RM283.33 million, on the back of a 55% increase in revenue to RM2.89 billion. This was mainly due to higher aluminium prices and production output from its new Phase 3 smelter, which achieved full commissioning in mid-October.

In a Nov 30 note, Hong Leong Investment Bank Research (HLIB Research) says it believes Press Metal is on track to recording its best-ever annual profit in FY2021, with a potentially stronger showing in FY2022.

“With demand remaining healthy while supply will be capped, we are still upbeat on our initial thesis on the sustained bull run in global aluminium prices over the next 12 to 18 months,” says the research house.

It has a “buy” call on Press Metal, with a target price of RM7.25. The stock had gained 28% this year to close at RM5.35 last Tuesday, giving the company a market capitalisation of RM42.7 billion.

It was, however, a tough quarter for CIMB Group Holdings Bhd, which slipped into the red with a net loss of RM100.59 million in 3QFY2021 compared with a net profit of RM194.44 million in 3QFY2020, mainly due to a RM1.22 billion impairment of goodwill recognised in the quarter related to the group’s Thailand business. Nevertheless, the banking group says the impairment has no impact on its capital and liquidity position, and will help optimise its return on equity (ROE) going forward, which will benefit shareholders.

Glove maker Top Glove Corp Bhd, which reported stellar earnings last year thanks to the pandemic, saw its net profit plunge 48% y-o-y to RM607.95 million in its fourth financial quarter ended Aug 31, on the back of a 32% decline in quarterly revenue to RM2.12 billion. This was due to normalising demand, following the mass vaccine rollout on a global scale, leading to lower sales volumes and ASPs, which were not matched by a corresponding reduction in raw material prices. Its performance was also affected by the Enhanced MCO, during which the glove industry in Selangor was not allowed to operate for 10 days — affecting 50% of Top Glove’s factories — as well as a subsequent round of MCO when the affected facilities were only permitted to operate at 60%.

BIG-CAP COMPANIES

(MARKET CAPITALISATION OF RM1 BILLION TO UNDER RM10 BILLION)

YTL Corp Bhd saw its earnings shoot up to RM105.22 million in its first financial quarter ended Sept 30 (1QFY2022) from RM1.29 million a year earlier, while revenue grew 21% y-o-y to RM5.06 billion. The significant increase in revenue and profit stemmed from its property investment and development segment, which saw sales of land by its subsidiaries Satria Sewira Sdn Bhd and Emerald Hectares Sdn Bhd. In November last year, the group via its subsidiaries sold two parcels of land in Bentong, Pahang, to Tropicana Corp Bhd for RM402.49 million. The transaction was completed in August this year.

Pharmaniaga Bhd, meanwhile, saw its 3QFY2021 net profit catapult to RM49.83 million from RM1.44 million in 3QFY2020, on the back of a phenomenal, more-than-threefold increase in revenue to RM2.13 billion, from RM624.8 million a year ago. This was mainly contributed by the group’s non-concession business, due to the sales of the Sinovac Covid-19 vaccine to the Ministry of Health as well as the private sector.

In a note last Thursday, HLIB Research reiterated its “buy” call on Pharmaniaga, with a target price of RM1.04. The research house continues to like the stock for the plans that the pharmaceutical company has that will help reduce its reliance on its existing concession business. These include the supply of vaccines to both the public and private sector in Malaysia, the export of the Sinovac vaccine and the group’s venture into the manufacturing of halal vaccines and insulin.

Pharmaniaga’s share price had declined 14% YTD to close at 84 sen last Wednesday, valuing the company at RM1.09 billion.

Higher CPO and PK prices also helped boost the earnings of plantation companies United Malacca Bhd — which reported more than a fivefold increase in net profit to RM20.85 million in its first financial quarter ended July 31, from RM3.55 million a year earlier — and Boustead Plantations Bhd, which also recorded more than a fivefold increase in its 3QFY2021 net profit to RM95.56 million from RM17.97 million a year earlier. FGV Holdings Bhd saw its 3QFY2021 net profit almost triple to RM399.39 million from RM136.89 million a year ago, thanks to higher CPO prices.

Meanwhile, Affin Bank Bhd saw its net profit for the quarter more than double to RM133.2 million from RM48.72 million a year earlier, thanks to improved net interest income, Islamic banking income, net fee and commission income, lower operating expenses and allowance for impairment losses.

CGS-CIMB Research said in a Nov 22 note that it expects Affin’s strong net profit growth to continue in 4QFY2021, driven by an improvement in net interest margin and lower loan loss provisions. Nevertheless, it retains its “reduce” call on Affin, with a target price of RM1.27, as it sees higher credit risks for the bank relative to its peers. This, says CGS-CIMB Research, is reflected in its high gross impaired loan ratio of 3.14% at end-September, which was double the industry’s average of 1.57%.

Affin’s share price had declined 7% YTD to close at RM1.67 last Tuesday, giving the bank a market capitalisation of RM3.5 billion.

Gamuda Bhd, which reported a quarterly loss of RM12.52 million in its fourth quarter ended July 31, 2020 (4QFY2020) as it took a one-off non-cash industrialised building system assets impairment of RM148.1 million, returned to the black in 4QFY2021, with a net profit of RM214.08 million, thanks to stronger construction and property earnings.

Meanwhile, it was a tough quarter for Sapura Energy Bhd, which reported a net loss of RM1.52 billion in its second quarter ended July 31 compared with a net profit of RM23.74 million a year earlier. The decrease was mainly contributed by provisions for foreseeable losses and higher project costs incurred for certain projects during the current quarter. Its revenue fell 38.7% y-o-y to RM747.11 million as a result of lower revenue recognised from its engineering and construction and operations and maintenance business segments, due to a lower percentage of completion during the quarter resulting from recognition of foreseeable losses and higher project costs.

Malaysia Building Society Bhd (MBSB) recorded a net loss of RM104.58 million in its third quarter compared with a net profit of RM258.24 million a year earlier. This was due to a higher net allowance for impairment charged on its corporate portfolio. The group also recorded a higher loss on modification of cash flow for 3QFY2021 following the moratorium granted to retail customers under the Pemulih package announced by the government.

In a Nov 30 note on MBSB, AmInvestment Bank maintained its “buy” call on the stock, with an unchanged fair value of RM1.08 per share, supported by an ROE of 9.5% for FY2022, pegging the stock to a price-to-book value of 0.8 times. It added that the valuation of the stock remains undemanding at 0.5 times FY2022 price-to-book value.

MBSB’s share price had declined 10% YTD to close at 59 sen last Tuesday, giving the company a market capitalisation of RM4.12 billion.

MID-CAP COMPANIES

(MARKET CAPITALISATION OF RM500 MILLION TO UNDER RM1 BILLION)

Comfort Gloves Bhd managed to triple its earnings to RM148.82 million in its second quarter ended July 31 from RM42.8 million a year earlier, on the back of more than a twofold increase in revenue to RM504.23 million. This was achieved mainly due to an increase in ASPs and higher sales volumes.

On its prospects, the group expects softer ASPs in its next financial quarter, but remains optimistic about its long-term prospects, with the commissioning of an additional seven double former dipping lines expected to be completed towards the end of its financial year ended Jan 31, 2022.

Steelmaker Hiap Teck Venture Bhd reported an almost sixfold increase in net profit for its fourth financial quarter ended July 31 to RM60.48 million, from RM10.29 million a year earlier, thanks to a sharp turnaround at its joint venture entity Eastern Steel Sdn Bhd because of higher steel prices. This was despite a 22% y-o-y decline in revenue to RM164.83 million that was due to the shortened operating period during the MCO.

Malaysian Bulk Carriers Bhd (Maybulk) turned in a net profit of RM113.58 million in 3QFY2021 compared with a net loss of RM5.95 million a year earlier, on the back of a 38% y-o-y increase in revenue to RM58.68 million, thanks to higher charter rates and lower operating expenses from having a smaller fleet.

Semiconductor automated test equipment manufacturer Aemulus Holdings Bhd reported an almost fourfold increase in net profit to RM4.07 million in its fourth quarter ended Sept 30, from RM1.04 million a year earlier. Revenue for the quarter more than doubled to RM17.3 million from RM7.2 million, thanks to strong demand for mobile devices and tablets, radio frequency (RF) filters and enterprise storage markets.

CGS-CIMB Research in a Nov 9 note reiterated its “add” call on Aemulus, with a target price of RM1.50, as it sees a new exciting growth driver for the company following its recent entry into the supply of RF testers for chips used in 5G network base stations in China. Aemulus’ share price had appreciated 82% since the beginning of the year to close at RM1.10 last Tuesday, giving the company a market capitalisation of RM679.6 million.

It was a tough quarter for convenience store operator myNEWS Holdings Bhd. Its net loss widened to RM14.92 million in its third financial quarter ended July 31 from RM6.09 million a year earlier, on the back of a 15% y-o-y decline in revenue to RM93.89 million. This was due to the MCO and EMCO, which mainly impacted the Klang Valley, where 80% of myNEWS outlets are located.

Automotive player Tan Chong Motor Holdings Bhd saw its net loss widen to RM44.2 million in 3QFY2021 from RM7.33 million a year earlier. It attributed the 55% y-o-y plunge in revenue to RM439.28 million to the movement restrictions in Malaysia and the Indochina markets in which it operates.

HLIB Research in a Nov 26 note maintained its “sell” call on the stock, with a target price of RM1, as it is relatively concerned about the continued stiff competition from domestic players, as well as the political uncertainty in Myanmar, where the group has operations.

Tan Chong’s share price had declined 10% YTD to close at RM1.11 last Tuesday, giving the company a market capitalisation of RM717.38 million.

SECTORS TO LOOK OUT FOR IN 2022

Private investor and former investment banker Ian Yoong Kah Yin sees bright spots in the logistics and consumer discretionary sectors next year.

“The logistics sector is attractive as supply chain bottlenecks and disruptions have increased the pricing of logistics services. The problems are not expected to abate over the next 12 to 18 months. Earnings for the logistics sector are expected to grow by 18% to 25% in 2022,” he tells The Edge.

“The consumer discretionary sector is [another] compelling investment proposition. The Covid-19 pandemic has badly impacted many retail businesses. Many have had to close permanently. Anecdotal evidence indicates that a substantial percentage of the competition [mainly unlisted] was eliminated in 2020 and 2021. This is positive for retail businesses that managed to survive and continue operating.

He adds that the oil and gas (O&G) sector, which has been in the doldrums for the past five years, could start to look attractive too. “While there are balance sheet risks for selected O&G stocks, the rest of the listed companies should outperform as Petroliam Nasional Bhd increases its capital expenditure (capex) for 2022. Petronas plans to allocate an average of RM20 billion for capex in upstream activities between 2022 and 2027. The O&G sector will most likely benefit from an upturn in the global capex cycle,” he says.

Yoong believes there could be interest in companies that have made a bid for a digital banking licence in Malaysia, which is expected to be given out in 1Q2022. “We anticipate speculative interest in listed companies that are in consortiums that have applied, or are planning to apply, for the digital banking licences.”

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.