This article first appeared in The Edge Malaysia Weekly, on October 19 - 25, 2015.

Amid concerns over whether the El Niño effect will be severe and the rebound in crude palm oil (CPO) prices sustainable, TSH Resources Bhd sees better days on the horizon.

Whether or not CPO prices make a marked recovery, the Sabah-based planter is confident of bumper crops ahead that will boost its earnings significantly. Its young trees will reach peak production in the next three to five years, which means the group will have more palm oil to sell.

and Aik Sim believe that in the longer term, CPO prices will strengthen as global demand for palm oil grows")

“We have done all the hard work and the next three to five years will be when we will achieve a steady income stream,” group managing director Datuk Tan Aik Sim tells The Edge in an interview.

TSH (fundamental: 0.30; valuation: 0.50) has been religiously following a planting schedule of between 4,000ha and 5,000ha every year.

As a result, it enjoys consistent production growth as there is always a steady number of trees reaching maturity each year.

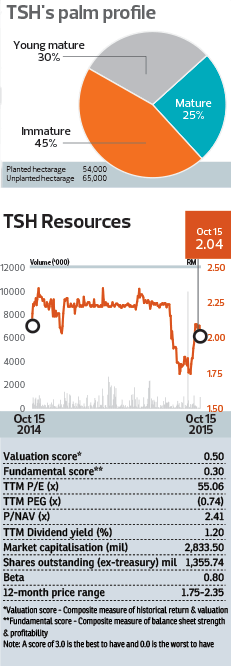

Currently, the group’s 54,000 planted hectares in Sabah and Kalimantan, Indonesia, have an average age of five to six years. Some 45% of the palms are immature and 30%, young mature.

“Our profit will probably more than double in the next two to three years, even at current CPO prices. If prices go up, it will be fantastic,” says Aik Sim’s brother, chairman Datuk Kelvin Tan.

With CPO prices constantly struggling to breach the RM2,500 level in addition to a stubbornly high inventory level, Kelvin is probably the rare optimist, given that most plantation companies, including TSH, have seen a big drop in earnings.

The benchmark three-month futures contract spent much of the year averaging about RM2,200 per tonne, a far cry from the RM3,000 to RM4,000 levels before the commodity boom ended in 2012.

CPO traded in the RM2,000 to RM2,300 range this year, and then slid to a low of RM1,867 following a worldwide rout in August.

Renewed talk of a possible El Niño sent prices back up to more than RM2,400, but most analysts believe this is probably the highest the prices would go amid competition from soybean oil. Last Friday, the benchmark contract closed at RM2,302.

While the Tan brothers are usually reluctant to predict CPO prices, they believe that in the longer term, prices will strengthen as global demand for palm oil grows.

The growing population and burgeoning middle class in countries like China and India could mean a higher consumption of palm oil. “We also noticed that Indonesia’s plantings have halved in recent years and this points to a structural deficit in the future,” says Aik Sim.

Whatever the case, TSH remains fairly insulated from CPO price fluctuations due to its ability to keep the cost of production low — something the management has been proud of.

Despite the rising cost of inputs like fertilisers and labour, the group’s cost of production last year was RM890 per tonne. The Malaysian average is RM1,200 to RM1,500 per tonne at the moment.

That said, TSH could not escape the downward trend in the industry’s earnings. The group’s earnings took an unusual hit from the unfortunate confluence of factors in the first half of its financial year ending

Dec 31, 2015 (1HFY2015).

Net profit dropped to RM13.5 million from RM87.6 million a year ago while revenue slipped 30% to RM412.2 million. The obvious culprit was a 14% decline in the average CPO selling price to RM2,152 in 1HFY2015 from RM2,501 in FY2014.

The decrease in earnings was also attributed to a lower fresh fruit bunch production of 297,221 tonnes compared with 319,417 tonnes a year ago, due to a drought in Kalimantan last year.

Core operating profit halved to RM57.8 million, after booking RM34 million on unrealised foreign exchange losses.

In FY2014, net profit stood at RM125.5 million on revenue of RM1.08 billion, compared with a net profit of RM151 million on revenue of RM1.02 billion in FY2013.

While 2015 is shaping up to be worse than expected for TSH, Kelvin points out that the group still made a respectable profit in 1HFY2015 and it will remain focused on growth.

“We still have land to continue planting to maintain growth even for the next 10 years. Over the next few years, as we gain a stronger and better financial position, we may increase our yearly planting target,” he says.

TSH still has some 65,000ha of greenfield land available for planting — the product of an aggressive acquisition trail over the last few years.

This year, it made two more acquisitions — 9,000ha in Kalimantan and 5,000ha in Sabah.

“For the next 5 to 10 years, we want to focus on Sabah and Indonesia,” says Kelvin.

Land scarcity is becoming a reality, and although TSH continues to look, Kelvin admits that good land is difficult to come by.

But TSH can afford to slow down its buying spree. At its current rate of planting, its landbank can last another 13 years, time enough to clean up its balance sheet.

As a fairly young plantation company — 18 years — TSH has had to gear up to finance its acquisitions. As at June 2015, it had RM1.17 billion in net debt, translating into a gearing ratio of 0.94 times, a level it is comfortable with as long as it does not exceed a ratio of one.

“We try to strike a balance between gearing and growth. As income increases in the next few years, we will pare down our debt to about 0.6 times gearing,” says Kelvin.

For investors, it is of interest that TSH intends to maintain dividends at about 30% of net profit (FY2013: 30%; FY2014: 27%).

When TSH’s oil palms reach their prime and production peaks, its dividend would grow in tandem, but investors have to be patient for a while.

TSH’s shares were trading sideways for most of the year — between RM2.20 and RM2.30 — but plunged 21% in end-August to RM1.75 as a selldown swept across global equity markets.

The stock rebounded to RM2.04 last Thursday, giving the group a market capitalisation of RM2.83 billion.

Despite the relatively young age profile of TSH’s plantations, investment analysts are not as excited as the Tan brothers about its earnings prospects as most of them are still cautious about the plantation sector.

For the analysts tracking the group, TSH appears fully valued, based on their 12-month target price of RM2.05, according to Bloomberg data.

MIDF Research has the highest target price of RM2.33 (14% upside) while KAF Seagroatt & Campbell Securities has the lowest target of RM1.80 (11.7% downside).

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.