This article first appeared in The Edge Malaysia Weekly on February 13, 2023 - February 19, 2023

WHEN it comes to investing in the stock market this year, plantation counters are likely to rank fairly low on investors’ lists. According to projections, demand for crude palm oil will not be strong, considering the high inventory of vegetable oils in the major markets of India and China.

However, some plantation companies are forecast to distribute good dividends over the next 12 months, resulting in decent dividend yields on their stocks, especially if investors buy them at the current low prices.

Private investor and former senior investment banker Ian Yoong Kah Yin says the good dividend yields of 4% to 5% will provide a floor for the share prices of the various plantation companies. “Plantation stocks (with good dividend yields) will be attractive to investors, particularly institutional funds, as they are drawn to the attractive yields and the limited downside of plantation stocks (because the dividend yields provide a floor for the share price).”

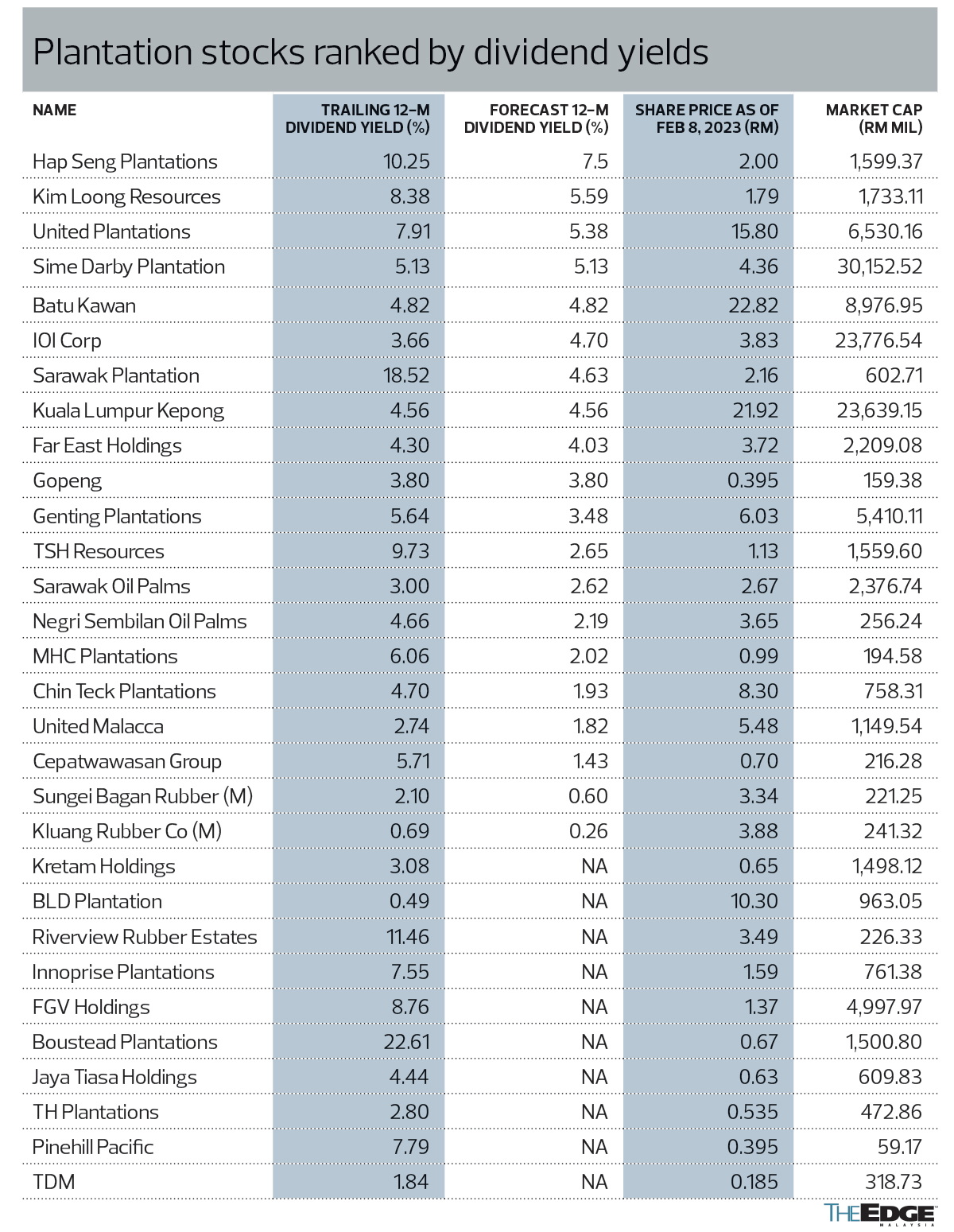

Out of the 30 plantation stocks on Bursa Malaysia selected by The Edge, nine have attractive dividend yields based on their share prices as at last Wednesday, and their median dividend per share over the next 12 months as forecast by analysts.

These are Hap Seng Plantations Holdings Bhd, which is trading at a forecast dividend yield of 7.5%, Kim Loong Resources Bhd (5.6%), United Plantations Bhd (5.4%), Sime Darby Plantation Bhd (5.13%), Batu Kawan Bhd (4.82%), IOI Corp Bhd (4.7%) and Sarawak Plantation Bhd (4.62%).

Others include Kuala Lumpur Kepong Bhd (KLK) with 4.56% and Far East Holdings Bhd with a forecast 12-month dividend yield of 4.03%, based on their share prices last Wednesday.

To be sure, many plantation stocks had offered good dividends over the last 12 months, owing to the super profit they enjoyed in the early part of the year when CPO prices were high.

For example, Boustead Plantations Bhd’s (BPlant) trailing 12-month (TTM) dividend yield is 22.6%, while Riverview Rubber Estates Bhd was trading at an 11.5% TTM dividend yield as at last Wednesday. TSH Resources Bhd’s TTM dividend yield is 9.73%.

However, it is highly unlikely that most plantation stocks will repeat last year’s performance in 2023, as the average CPO price is expected to hover around RM3,800 per tonne, compared with the average of RM5,126 per tonne in 2022.

“I don’t cover BPlant per se, but I should think that if a company follows its dividend policy, which would result in a high dividend yield this year, then it should be fine to buy into those stocks,” Hoe Lee Leng, head of regional plantation at RHB Research, tells The Edge.

Nevertheless, she says, investors should bear in mind that most plantation groups are already at the tail end of their respective financial years, so whoever buys into a stock now may not be getting the full dividend yield that had been declared over the last 12 months.

Most research houses have a “neutral” call on the plantation sector, due largely to the expected weaker demand and stronger production, especially in the second half of this year, but supported by changes in the tax structure in Indonesia as well as the country’s biodiesel mandate.

At the same time, the inventory of vegetable oils is still high in India — the world’s largest consumer of vegetable oil including palm oil — while China is ramping up its soybean oil production to reduce dependency on foreign producers such as the US and Brazil.

Despite the “neutral” outlook on the sector, a few names keep popping up as the top picks of research houses. These are KLK, TSH, Hap Seng and IOI, with FGV Holdings Bhd sometimes thrown into the mix. In a Jan 31 note, RHB Research says planters such as KLK, IOI, Sime Darby Plantation and FGV, which undertook more aggressive forward selling activities, should be able to recognise better CPO prices than their peers in the fourth quarter of 2022.

Meanwhile, Teh Kian Yeong, plantation analyst at Kenanga Research, says in a Jan 11 note that the research house prefers counters with the ability to expand upstream, such as KLK and TSH, with the latter having substantially recapitalised and proceeding to expand its planted area from 40,000ha to 60,000ha.

Teh adds that for investors prioritising yields, Hap Seng looks attractive.

RHB Research has a target price of RM27.85 for KLK while Kenanga ascribed a fair value of RM25.50 with an “outperform” call on the counter. RHB Research is calling a “buy” on IOI with a target price of RM4.60 per share, while UOB KayHian has a RM4.80 target price on the stock.

Kenanga assigned an “outperform” call to TSH with a target price of RM1.35, while TA Securities has a RM1.34 target price with a “buy” call on the stock. TA Securities is also calling a “buy” on FGV with a target price of RM1.56.

Meanwhile, an executive with an integrated plantation group says the lower CPO price would benefit the downstream segments of integrated plantation players as the feedstock price would be lower. However, in the short term, the CPO price should be well supported, he says.

“Of course, the challenge right now is the price, which has come down below RM4,000. Especially for pure-play plantation companies, this is a challenge. For integrated groups like us, our downstream will benefit and provide a natural hedge to our upstream.

“The upcoming festive season of Ramadan, as well as the Indonesian biodiesel mandate increasing to 35% and the easing of the Covid-19 restrictions in China will provide some support to the CPO price,” he adds.

KLK, IOI and Sime Darby Plantation are among the integrated plantation players with significant downstream segments.

KLK’s downstream manufacturing segment contributed 32.8% to the group’s results in the financial year ended Sept 30, 2022, while IOI’s resource-based manufacturing segment contributed 20.4% to the group’s results for the financial year ended June 30, 2022.

Sime Darby Plantation’s downstream segment contributed 27.3% to the group’s results for the nine-month period ended Sept 30, 2022.

Most of the research houses were “neutral” on Sime Darby Plantation. UOB KayHian has a “hold” call with a target price of RM4.75, while TA Securities ascribed a value RM4.69 on the counter. RHB Research has a target price of RM4.60 per share.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.