This article first appeared in The Edge Malaysia Weekly, on December 14 - 20, 2015.

EDRA Global Energy Bhd president and executive director Datuk Mark Ling is breathing easier now compared to a year ago when he was thinking hard about how to raise the much-needed fresh capital to ease the company’s tight cash flow and to kick-start power projects that have been granted by the government.

EDRA Global Energy Bhd president and executive director Datuk Mark Ling is breathing easier now compared to a year ago when he was thinking hard about how to raise the much-needed fresh capital to ease the company’s tight cash flow and to kick-start power projects that have been granted by the government.

New shareholder China General Nuclear Power Corp Ltd (CGN) is going to pump

RM10 billion into Edra for expansion locally and abroad after paying RM9.83 billion cash for the takeover and assuming Edra’s net debt of RM6.8 billion.

Having RM10 billion fresh capital was something Ling could only dream about when Edra’s outgoing shareholder, 1Malaysia Development Bhd (1MDB), sank deeper into a financial quagmire with debts ballooning to over RM45 billion.

Like it or not, CGN, whose debt papers are rated A3 by Moody’s, is perceived to be in a better position to grow Edra. Tenaga Nasional Bhd (TNB) was defeated by the Chinese state-owned energy group in the bid for Edra.

In an interview with The Edge, Ling starts off by refuting the speculation that his team was handsomely rewarded for concluding the sale of Edra.

“Contractually, there are no entitlements or bonuses for the management for [successfully] selling Edra. However, my team has really put in their best effort over the past year and I believe they are deserving of a fair reward,” says Ling, whose first task when he joined the company in October last year was to list Edra on Bursa Malaysia.

The initial public offering did not materialise, although its rival Malakoff Bhd, which had delayed such an exercise for at least three years, managed to raise RM3.6 billion this year.

Ling, 53, is probably facing a different sort of stress now — the challenge to deliver returns to shareholders once things are moving in Edra.

He says the team won’t have much time to waste. They will have to figure out ways to double Edra’s current installed capacity in order to earn the lucrative returns that the Chinese shareholder is expecting.

“Our very first task under CGN will be to secure and enlarge our footprint with more power assets. We are looking at about 5,000mw of new projects outside the country,” says Ling.

“When you acquire a power company, you aren’t just buying the existing assets. You are buying it for the assets that it can bring you in the future.”

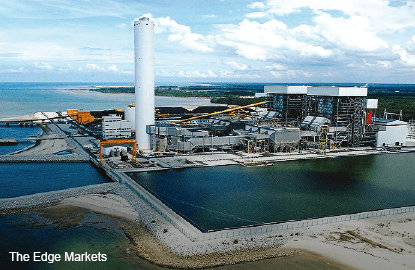

For expansion in Malaysia alone, CGN is expected to inject RM5 billion to get the projects off the ground. There will not be a repeat of Project 3B — the 2,000mw coal-fired power project that Edra was forced to sell to TNB because it lacked the capital to develop it.

All in, CGN is expected to inject over

RM10 billion to ensure that Edra can continue expanding. In contrast to CGN’s estimated total asset value of RMB398.47 billion (RM266.4 billion), the sum is small. For perspective, CGN’s installed capacity of over 25.4gw (25,400mw) is almost five times Edra’s. In fact, the group has almost 40gw of capacity, including 13.8GW of nuclear power capacity that is already under construction.

This does not include the 2,500mw to 2,900mw worth of Malaysian projects that Edra is already sitting on — the 2,000mw to 2,400mw combined cycle gas turbine (CCGT) Project Tuah (also known as Project 4B) and up to 500mw solar capacity, of which 50mw has already secured a power purchase agreement.

Conversely, one may wonder what value a group like CGN may see in Edra. Interestingly, despite CGN’s size, Edra is the largest acquisition of foreign power plants it has ever done. To date, CGN owns 2,213mw of capacity outside of China — in France, South Korea, the UK and Australia.

But more importantly, Edra could be CGN’s best chance to expand its reach outside of China.

“By acquiring Edra, CGN instantly gained access to not just one market, but four — Egypt, Malaysia, Bangladesh and, indirectly, Pakistan. But that isn’t all. We Malaysians, uniquely, have a strong acceptance in other countries quite easily. We can go into markets that the Chinese, traditionally, would have struggled,” says Ling.

Projects in Egypt especially, where there is a shortage of power, will be able to drive most of Edra’s expansion in the near future, he adds. With CGN backing up Edra’s well-established presence in Egypt — inherited from Tanjong Power (then known as Powertek under 1MDB) — he is optimistic about Edra’s prospects there.

More importantly, CGN isn’t just interested in Edra’s hard assets and power contracts. It wants to tap Edra and Malaysia’s talent pool.

“Between TNB as a training ground and the private sector with the IPPs (independent power producers), we have developed a very strong pool of professionals in the power business. The Chinese want our people,” says Ling.

Hence, despite the change in ownership, Edra’s management and staff will not have to worry about job security.

“CGN has indicated very clearly to us that there will be no job cuts. In fact, it intends to leave the management intact. They are only proposing to introduce two personnel — one into finance and another into operations,” says Ling, dismissing concerns that CGN may trim headcount to reduce costs and improve efficiency.

According to him, CGN has done a detailed study on Edra’s power assets, including its cost structures.

To recap, CGN’s Hong Kong-listed unit CGN New Energy Holdings (formerly known as CGN Meiya Power Holdings Ltd) was the initial vehicle to be deployed for the takeover.

“CGN has already studied our operations and the costs, and it is comfortable with them. They have made sure that the operations are sustainable. Traditionally, companies like Tanjong plc, Genting Bhd and Jimah [Energy Venture Sdn Bhd] already have very conservative cost structures. They are very much low-cost operators,” Ling explains.

Case and point: Edra has already put out advertisements seeking to hire up to 30 people to support the group’s plans for rapid expansion.

According to Ling, Edra is wrapping up the land acquisition for both the solar project in Kedah and Project Tuah in Melaka. In fact, the engineering, procurement and construction (EPC) contracts for Project Tuah are underway and bids will close on Feb 5. The EPC bids for the solar project are now under evaluation.

On that note, Ling ensures that CGN will not prioritise Chinese EPC contractors. “Principally, CGN is not allowed to help out fellow state-owned enterprises. They want to keep it strictly to business. No favours, no country comradeship. Any contracts we give out will have to be done strictly on merit.”

For the Project Tuah tender, for example, he points out that there are no Chinese EPC contractors involved. Only Germans, Americans and Japanese are vying for that job, he says.

Looking ahead, the only major housekeeping that Edra needs to do with its balance sheet is the refinancing of some debts tied to Jimah power station that have high interest rates of up to 18%. If these debts can be refinanced, it would drastically improve Edra’s cash flow.

This time round, however, Edra’s funds won’t be spent on servicing debts borne by its parent. Instead, it will be reinvested to grow the business and create value, albeit for CGN.

Having an IPO is one option CGN could explore to unlock its investment values. When that happens, Malaysians would find out how lucrative these power assets could be if they are managed properly.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.