This article first appeared in The Edge Malaysia Weekly on March 21, 2022 - March 27, 2022

IN 2021, Malaysia’s approved foreign direct investment (FDI) amounted to RM208.6 billion, roughly three times more than the RM64.2 billion achieved in the previous year, the Malaysian Investment Development Authority (Mida) announced recently.

It is worth noting that the net FDI inflows in 2021 have rebounded to RM54.91 billion, the highest since pre-pandemic days. In 2020, net FDI inflows totalled RM14.64 billion while they came in at RM32.36 billion in 2019.

However, whether Malaysia can achieve such a performance this year, following 2021’s stellar numbers, “would be difficult” admitted Senior Minister (International Trade and Industry) Datuk Seri Mohamed Azmin Ali during the Mida Annual Media Conference 2022.

While it is understood that FDI helps to develop the economic sectors of a country and are deemed important to developing nations such as Malaysia, one question that often comes up is whether, in its attempts to attract FDI, the country is giving away too many incentives, resulting in foreign companies paying lower taxes than local ones.

A paper published by the International Journal of Research in Business Studies and Management in 2019 seems to suggest that it could be the case. It provided evidence that multinational corporations (MNCs) in Malaysia had a lower effective tax rate than the general prevailing corporate income tax rate, by 3.6%.

KPMG Malaysia head of tax Soh Lian Seng points out that MNCs could also have the opportunity to reduce their tax burden through a wide range of incentives. “MNCs with greater pre-tax income have more incentives and resources to engage in effective tax planning to reduce their tax liabilities, which will result in lower effective tax rates (ETRs).”

Profitable MNCs can efficiently utilise tax deductions, such as the double deduction in terms of R&D expenditure, promotion of exports, brand promotion activity, freight charges and employee training programmes,” he says.

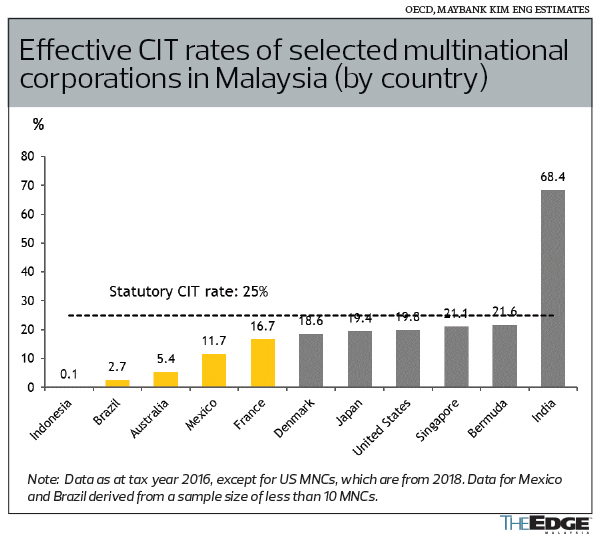

Soh adds that the results in the paper published by the International Journal are consistent with a study done by Maybank Investment Bank Research back in 2021, where the statistics showed that most foreign MNCs in Malaysia paid a lower effective corporate income tax (CIT) rate than the headline 25% rate, except for Indian firms.

The report sees a similar trend among neighbouring countries, where foreign MNCs in Singapore and Thailand largely enjoy low ETRs, or below the statutory rates of the respective countries.

Nevertheless, others highlight that lower ETRs do not only apply to MNCs but to any company that enjoys tax incentives.

“The effective tax rate of companies enjoying incentives is generally lower than those that are not. The existing incentive framework in Malaysia is non-discriminatory and incentives are granted to all eligible companies incorporated in Malaysia, including small and medium enterprises (SMEs). As long as a company undertakes incentivised activities, regardless of whether it is an MNC or FDI, and meets the conditions for the incentive, it will be eligible for the incentive,” says Deloitte Malaysia government grants and incentive leader Tham Lih Jiun.

As for whether providing MNCs with tax incentives would be a loss of revenue for the government, EY Asean tax leader and partner Amarjeet Singh believes it would depend on the type of investors. He says it is crucial to develop an understanding of what motivates investors to invest in a certain jurisdiction.

Potential resource- or market-seeking investors will generally invest in a country regardless of whether incentives are offered to them, says Amarjeet. In such instances, incentives are less of a key consideration in determining whether or not to invest.

On the other hand, investors who are efficiency-seeking and strategic-asset-seeking may require incentives to invest in a particular jurisdiction if they are not able to avail themselves of the balance of efficiencies when compared with other jurisdictions, he adds.

Simply put, efficiency-seeking FDIs are investments that look for factors such as low logistical and labour costs and plentiful supply of skilled labour to improve its competitiveness in the global market. They tend to be export-oriented industries.

Strategic-asset-seeking FDIs tend to involve mergers and acquisitions in order to own certain assets to compete in particular markets.

“In the case of granting incentives to attract investors who are efficiency-seeking or strategic-asset-seeking that would otherwise not have invested, then it is not really revenue forgone to the government,” says Amarjeet.

“On the contrary, such investments would generate multiplier economic benefits, for example, job creation and demand for local supplies and logistics. These activities would in turn generate tax revenue. There would also be other benefits to Malaysia, such as a transfer of technology and knowledge to the country as well as the upskilling of Malaysian workers.”

Global minimum tax, time for reform

However, with the Organisation for Economic Cooperation and Development’s (OECD) proposal to impose a global minimum tax beginning next year, using tax incentives to attract investment may not be as straightforward as it seems to be. Hence, it could be timely that Malaysia undergoes a comprehensive review of its tax incentive framework.

The process, which started in 2020, aims to ensure that tax incentives offered to foreign and local investors remain relevant to the current business landscape while maintaining the country’s competitiveness in attracting quality investments.

In a previous interview with The Edge, Finance Minister Tengku Datuk Seri Zafrul Aziz mentioned that the review of the tax incentive framework is expected to be finalised this year.

One of the initiatives on tax reform by the OECD is the BEPS 2.0 Pillar 2 measures, which is expected to change the global tax incentive landscape significantly.

The concept of global minimum tax will see foreign MNCs having to pay additional tax in their home countries if they enjoy tax incentives that result in them paying less than 15% tax. The Pillar 2 measures would apply to MNCs that have a group turnover of €750 million and above.

“This creates a new level playing field when it comes to attracting FDIs that would fall under the net of BEPS 2.0 Pillar 2 measures, which in a way reduces the race down to zero. Given the more limited room for highly attractive fiscal incentives, countries — including Malaysia — will have to continue building on other non-tax differentiators to remain as a competitive destination for investments,” says PwC Malaysia tax leader Jagdev Singh.

Nevertheless, Tham believes that tax incentives will still be relevant as not all companies will fall under the BEPS 2.0 Pillar 2 measures.

“The global minimum tax includes ‘substance carved out’ in computing the minimum tax rate. Malaysia may consider working with the relevant parties to draw up a policy for investment that has economic substance where the global minimum tax rules do not apply,” he adds.

“After all, the principle of the global minimum tax is to prevent artificial shifting of profits to low tax jurisdictions, and genuine investments with economic substance should not be part of that scope.”

Therefore, with the changes happening globally, there is certainly a need for Malaysia to look into its existing tax incentive structure to see whether it is still relevant.

“The global tax reform led by the OECD should not result in incentives no longer being relevant. Incentives, fiscal and non-fiscal, will continue to play a part, especially among Asean countries, as we compete to attract and retain FDI,” says Amarjeet.

“In this regard, and bearing in mind that the proposed implementation of Pillar 1 and 2 of the OECD’s BEPS 2.0 project in 2023, Malaysia’s tax incentive framework should be reformed to be more nimble and flexible, with the agility to pivot in tandem with the latest international tax policies and investor needs.”

Jagdev hopes that the reform will result in a holistic change in the tax incentive framework where tax incentives are granted on an outcome basis, where the level of incentive is closely linked to the delivery of the outcomes critical to the country. He believes the global minimum tax measures may result in tax holidays for companies being less relevant and hopes that the government will introduce innovative tax incentive mechanisms that will be crucial in differentiating Malaysia from its neighbouring countries.

“At the end of the day, tax incentives are only one part of the equation. With the changing global tax landscape, countries will have to work on a holistic approach to differentiate themselves in areas that are crucial to investors and being very focused on investments that are strategic to the economy,” he says.

Tham sees a more practical aspect of things, as he believes that the tax incentive reform should also result in a consolidation of the incentive process and approval under one agency so as to provide clarity to investors and avoid duplication of incentives.

“One of the challenges often faced by investors is navigating the various investment promotion agencies for different incentives and investment locations in identifying the most relevant incentives for them,” he explains, adding that this may not provide a cohesive front when promoting Malaysia as a preferred destination for FDIs.

KPMG Malaysia’s Soh believes that creating an efficient tax incentive system that is simple, transparent and automatic would remove uncertainty and be relatively easy to enforce. “This could potentially include a more straightforward or integrated platform and accelerated processing time for the application of the tax incentives and business licences,” he suggests.

“Incentives offered should be easily adopted without burdensome administrative application procedures. Perhaps online applications and expedited approval based on a fixed set of criteria may be considered for certain tax incentives, such as incentives targeted at SMEs.”

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.