This article first appeared in Personal Wealth, The Edge Malaysia Weekly, on October 26 - November 1, 2015.

Local special purpose acquisition companies are an alternative investment for those looking for decent returns with low risk. Nevertheless, investors should keep in mind the outlook for the oil and gas industry and the risks associated with it.

BURSA MALAYSIA-listed special purpose acquisition companies (SPACs) could potentially provide investors with a decent return with relatively low risk in the medium term, even as the oil and gas sector faces a down cycle and the stock market remains weak and volatile, say investment experts.

Gan Eng Peng, head of equity strategies and advisory at Affin Hwang Asset Management Bhd, believes the three “undergraduate” O&G SPACs could offer a good return over time. “All three SPACs — Reach Energy Bhd, CLIQ Energy Bhd and Sona Petroleum Bhd — could provide the same annualised return of about 13.5% if held to maturity,” he says.

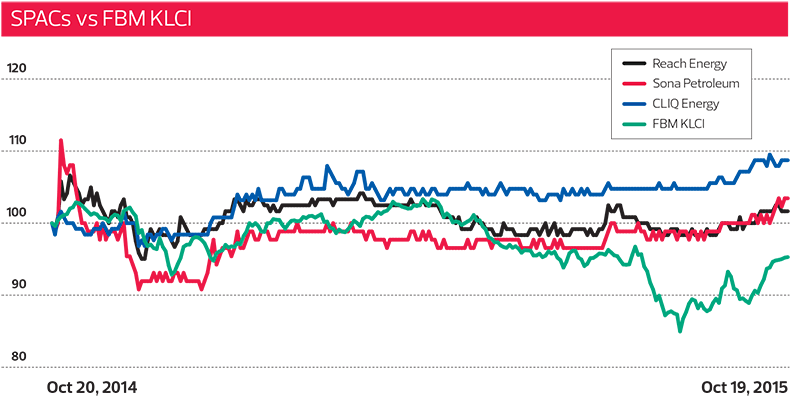

As at Oct 19, the share prices of CLIQ, Sona and Reach had surged 8.7%, 3.5% and 1.75% respectively over the last 12 months. All three stocks outperformed the FBM KLCI, which slid 4.9% to 1,718 points during the same period, and gave a return of 3.3% to 4%, which is higher than current fixed deposit rates.

Gan says these entities are a good investment for those who have a one or two-year horizon and are betting on the SPACs to fail. “Playing the cash arbitrage by buying into these SPACs and waiting for them to fail to acquire their qualifying asset (QA) or have their acquisition proposal rejected [makes for] a decent low risk investment,” he explains.

Critics say that betting on a SPAC to fail in its acquisition in order to benefit from the liquidating distribution is akin to gambling, but Gan says the investment is neither a gamble nor speculation.

“Even if the SPAC proposes to acquire an asset, the investor can reject the proposal and get back the cash held in trust. So, there is no speculative element,” he points out.

SPACs are given 36 months post-listing to secure a qualifying asset in order to “graduate” into a regular listed company. If they fail to do so, at least 90% of the proceeds from their initial public offering must be returned to investors.

Gan says investing in the current crop of SPACs is only viable if one takes the view that they will fail to acquire a qualifying asset and have to return the cash they hold in trust. “That is because the SPACs are trading at a discount to their cash value, which if held to maturity, is more than the returns from a fixed deposit or other low-risk investments.”

From a share price perspective, SPACs by their very nature should be trading at a discount to their cash value, owing to the risks involved. “They are after all buying assets at market value, so there is some risk of getting the assets as expected. There is also execution risk, given the thin management level and need to integrate the new assets,” says Gan.

“In an environment of abundant and cheap money, there are no big bargains to be found in most industries. The only exception is if the owners/management of the SPACs have an exceptional track record of buying and running businesses. Then, it might be worthwhile to take a long-term ride with them.”

Currently, the only viable investing strategy when it comes to SPACs is buying into new companies for their free warrants or buying into existing ones with the cash arbitrage angle in mind. “Investors seeking exposure to the O&G industry can find a lot more options out there, with battered share prices to choose from, from small to large caps,” says Gan.

Hong Leong Investment Bank (HLIB) analyst Jason Tan Yat Teng says in an Oct 19 research report that CLIQ and Sona, whose three-year deadline falls on April 9 and July 29, 2016, respectively, will provide an upside of 4.8% and 6.3% to their cash value. “The annualised return is about 10.1% and 8.1%, which is significantly higher than the average fixed deposit rate of 3.2% per annum,” he adds.

The report also says Reach — whose three-year deadline ends in August 2017 — is trading at the highest discount compared with its peers. “Reach is trading at a discount of about 16% to its latest gross trust per share, mainly due to its longer maturity date.

“If it manages to secure a QA in the near future, we expect the share price to trade at least close to its gross trust per share of 71.1 sen during its IPO, which should provide an immediate return of 16%. For investors with low risk appetite and longer investment horizon [can hold until maturity], Reach provides an annualised return of 12.6% per annum.”

In his earlier report, dated July 20, Tan says the SPACs’ gross trust value should serve as the base value, as investors can choose to vote against the QA and get back the cash value from the trust account plus net interest earned. The gross trust value refers to the total sum placed in the trust account. According to the Securities Commission Malaysia’s (SC) equity guidelines, a SPAC must place at least 90% of the gross proceeds raised from its IPO in a trust account.

The money in the trust account may be invested in permitted investments and any income generated by the funds, including interest or dividend income, must be accrued to the account. The total sum in the trust account may be released by the custodian upon termination of the account. This could take place following the completion of the QA within the permitted time frame or upon liquidation of the SPAC if it fails to acquire a QA.

If investors are not confident in the company’s QA, they can exercise their right to vote against it at a shareholders’ meeting and have the cash value in the trust account plus the net interest earned returned to the shareholders. However, the resolution of the QA must have the approval of at least 75% of the shareholders.

Mixed outlook for SPACs

A local bank analyst says the prospects for these SPACs do not look good for the time being. Although oil prices have plunged more than 50% from their peak last year, it could be a risky investment for investors expecting a substantial return from a successful qualifying acquisition.

Brent crude oil plunged to a 6½-year low of US$42.69 a barrel on Aug 24 before rebounding to US$50.25 on Oct 19. The analyst says prices did not stay low long enough for SPACs to secure a QA.

“Yes, the plunge in oil prices has impacted the industry quite badly, but it has not yet prompted the sellers to drop prices. Asset owners, such as oilfield operators, still can’t agree on the pricing with SPACs. They think oil prices will rebound in the longer term,” he adds.

The analyst points out that the disclosure of the maturity date and cash available is another factor that puts SPACs at a disadvantage when the parties negotiate the acquisition price. “Everyone knows how much money you have. This makes the acquisition process tougher,” he says.

“The market sentiment on SPACs is not very good, unless another SPAC [after Hibiscus Petroleum] makes a successful QA,” he adds.

Reach managing director and CEO Shahul Hamid, however, says oilfield operators have already started to lower their pricing. “This is because we have to negotiate the price based on projections by industry experts. Let’s say, a majority of the experts says ‘Look, oil prices won’t reach US$100 a barrel within few years’, of course the sellers cannot say they are all wrong.

“There aren’t too many of them in distress out there, but it is a period of consolidation where more mergers and acquisitions are coming in. This is when the operators will try to rationalise their assets.”

Oil prices are expected to be at the US$70 to US$75 per barrel in the next couple of years, based on the company’s projection, says Shahul, 65, who has been in the O&G industry for the past 35 years, having worked with Exxon Mobil and Shell.

He also says that disclosing the amount of funds the SPAC has is not a disadvantage. “Not really, because they do know we can also have debt funding. So, they don’t really know our limits.”

Hibiscus Petroleum Bhd was the first SPAC to secure a QA and graduate into a regular listed company on the local bourse. This gave investor confidence a boost. But the sentiment has waned as the other three SPACs have yet to secure their QA.

In May, CLIQ entered into a sale and purchase agreement with Kazakhstan-based Phystech Firm LLP for the latter’s two producing onshore oilfield blocks for US$117.3 million (RM500 million). The purchase, which is expected to be completed by year-end, will see CLIQ control 51% equity interest in a special purpose vehicle under which the oil assets will be parked.

The weak ringgit has not spelt good news for SPACs like CLIQ as they may have to resort to bank borrowings if they are unable to fund their foreign acquisitions.

Save by subscribing to us for your print and/or digital copy.

P/S: The Edge is also available on Apple's AppStore and Androids' Google Play.